Blame the baby.

When we realized I would have to get up to snot suck our daughter’s nose in the middle of the night, we were worried she’d take forever to get back to sleep. Turns out, I’m the one who can’t get back to bed, which means another middle of the night post.

NBA free agency and my undying love for Vernon, BC are a few of the topics rolling around in the last few hours, in addition to the following thoughts:

1. I’m totally over the “Toronto is expensive/unaffordable conversation”. The impatience has been lingering for a while but was prompted over the weekend at a family outing to Ribfest, in Etobicoke, which btw, Billy Bones BBQ had the best ribs, in case you were wondering. While debating the other contenders, Lisa and I ran into some former downtown work colleagues, who now live a five-minute walk from the event location, Centennial Park. They’re the same vintage as us (“older” millennials) and made the decision to trade away the prospect of seven-figure debt, for longer commute times. They’re happy, they have space for their family, and plenty of park space and recreation in the surrounding area.

And that’s it. Nothing fancy.

There are dozens of reasonably priced communities all over the GTA and the country, how did we get to this insane point, where we forgot about them and settled on obsessing over just two?

2. I have quite a few clients who invest with Robo-advisors, which is perhaps a bit confusing since they’re supposed to offer…. “advice”? It’s not a blanket dig at Robos, but I genuinely think there’s an interesting question, how will fin-tech companies and their scale-to-infinity mentality, integrate non-scaleable services like advice and planning, which all result in negative economies of scale.

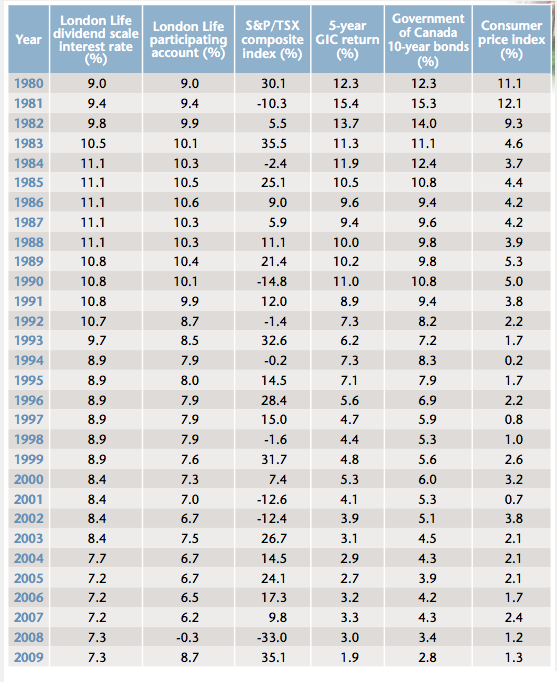

3. Yes, you need to consider after-tax returns when making investment decisions, but too many investors and their advisors are doing something which I’ll describe as prioritizing tax-minimization. For example, it’s fairly common to see portfolios with preferred shares (dividend income benefitting from the dividend tax credit) replacing fixed income (interest income taxed at your marginal rate). These are usually very conservative clients and when I ask why that decision was made, the answer is that they were told preferred shares are “risk-free, like bonds but at a lower tax rate”, which is less than accurate ...

4. Hey, DIY Investors guess what? You’re all really, really scared of Trump! Biggest piece of advice I can offer is, fairly boring - turn off the news and properly set your asset allocation. Most portfolios have done well over the last number of years, but everyone seems to be paralyzed by those gains and what to do with their super high equity allocations.

5. Thinking about how curated social media platforms like Instagram have become, got me thinking how we don’t share anything about money either online or IRL. I wrote a post last year covering some of my past investing mis-steps, https://www.youandyoursfinancial.com/insights-and-advice/2018/6/6/stupid-things, but it certainly feels like honest financial conversations need to happen more often.

6. I get asked every now and again what I am personally invested in and unfortunately I have a boring answer. It’s all cash at the moment, for a number of reasons. The biggest, was to have it available during the startup portion of this business, but as that progressed, my wife and I haven’t sat down to revise it. So there you have it, at the moment, the person who does Investment Plans, is without and updated one! It’s in the works, but again, this is the baby’s fault.